Abstract

This study investigates the emergence and impact of digital insurtech in addressing critical protection gaps faced by Ghanaian micro, small, and medium enterprises (MSMEs). Ghana’s large informal sector and high mobile money penetration rate provide a unique case for examining how technology is leveraged to design inclusive financial products. Employing a mixed-methods approach, the research analyzes localized data from the Bank of Ghana and the National Health Insurance Authority, alongside a case study of the AI-driven virtual insurer Hollard Ghana. Findings indicate that successful insurtech models prioritize contextual adaptability over technological complexity, embedding insurance within familiar digital platforms and social structures. Challenges persist, however, in data localization, trust-building, and regulatory evolution. The paper concludes with a replicable action guide for stakeholders, emphasizing the need for human-centered design, collaborative data ecosystems, and proactive, innovation-friendly regulation to fundamentally build economic resilience.

Keywords: Insurtech, digital finance, SMEs, financial inclusion, Ghana, mobile money, regulatory sandbox

1. Background

Ghana’s business landscape is defined by two powerful, contrasting forces: pioneering digital payment infrastructure and a vast yet fragile informal economy. This tension sets the stage for a transformative insurtech revolution

Figure 1: digital payment penetration vs. insurance coverage gap

The digital foundation is solid. By the third quarter of 2025, Ghana’s mobile money ecosystem ranks among the world’s most active. The Bank of Ghana reports over 46 million registered mobile money accounts, driving quarterly transaction volumes exceeding 450 billion cedis (approximately $35 billion)(Bank of Ghana) . This widespread adoption has accustomed millions to digital transactions, creating a ready-made channel for low-premium, high-frequency insurance products. Meanwhile, the government, through the Ministry of Finance, is drafting a ten-year development plan for the insurance sector. This explicitly acknowledges the industry’s role in economic resilience and signals a policy shift toward greater innovation (Ghana Ministry of Finance).

Beneath this digital surface, however, lies significant vulnerability. Small and medium-sized enterprises (SMEs), which account for over 90% of all businesses and contribute approximately 70% of Ghana’s GDP, remain dangerously exposed to various risks(Ghana Statistical Service). While the National Health Insurance Scheme (NHIS) is crucial, it faces coverage challenges. A 2025 study published in BMC Public Health revealed that only about 54% of the population holds valid NHIS membership, with informal workers severely underrepresented(Ofori, Ebenezer, et al). For these entrepreneurs, traditional commercial insurance remains largely inaccessible due to product complexity, stringent underwriting requirements for formal financial records, and high costs. This “protection gap” leaves the pillars of Ghana’s economy highly vulnerable to shocks from health emergencies, property damage, climate events, and supply chain disruptions.

2. Challenge

The primary obstacle to insurtech is not technical, but human—namely, building trust in a market wary of financial institutions and abstract promises. This underscores that innovation must first bridge the gap in perception and trust.

Figure 2: radar chart of insurtech adoption barriers

A related technical challenge is the data paradox. While digital payments generate vast amounts of data, this information is often siloed or unstructured for insurance purposes. Developing accurate, equitable risk models for informal sector workers—such as taxi drivers or tailors—requires moving beyond traditional credit scoring. Insurtech companies must innovate while utilizing alternative data—such as mobile phone credit purchase patterns and transaction histories—while navigating stringent data privacy concerns and the high costs of cleaning and integrating disparate datasets. Furthermore, heavy reliance on global or regional aggregated reports, rather than highly localized data, may result in products that fail to align with specific community risks—such as Accra market’s unique flooding patterns or the Upper East Region’s drought cycles.

3. Case

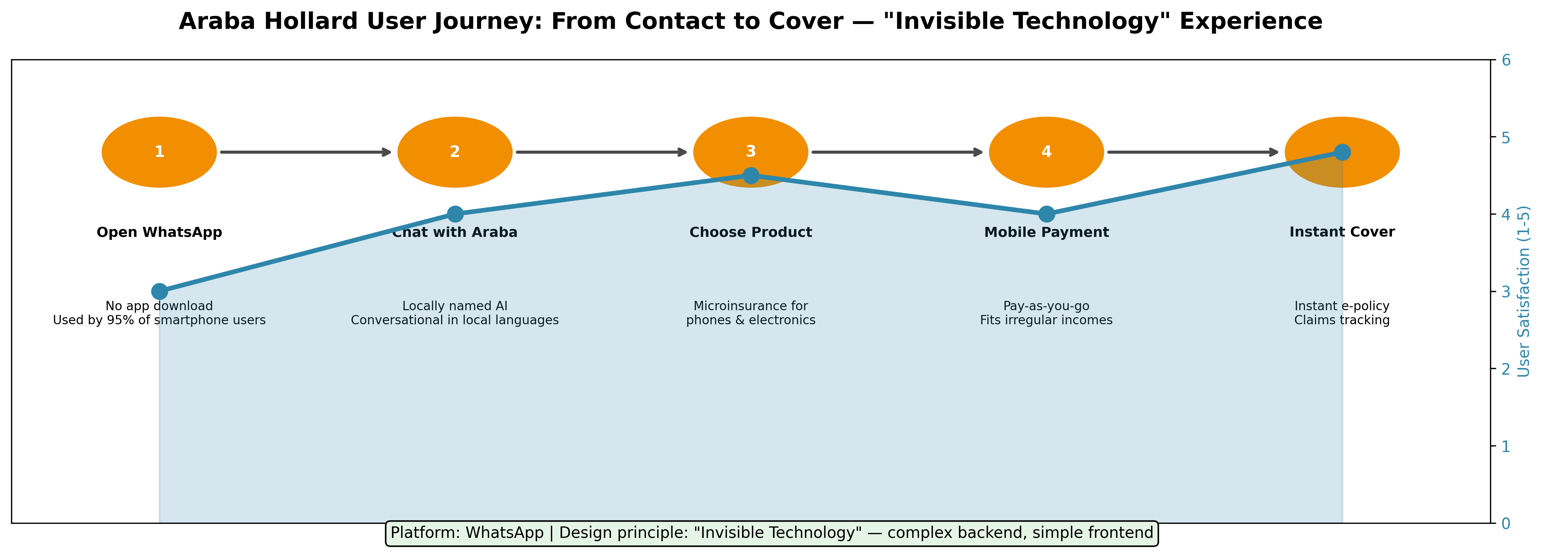

A prime example of contextual innovation is Hollard Insurance Ghana’s launch of “Araba Hollard,” West Africa’s first virtual insurance assistant on WhatsApp. This case exemplifies a strategic emphasis on cultural adaptability and meeting user needs where they are(Hollard Insurance Ghana).

Unlike developing a standalone app that requires downloading, consumes data, and demands learning a new interface, Hollard embedded its service within WhatsApp—a platform used daily by over 95% of Ghanaian smartphone users. This AI assistant, bearing a locally familiar name, guides users through simple conversational language to purchase and manage microinsurance coverage for assets like mobile phones or electronics.

Hollard also demonstrates strong cultural and contextual adaptability. It not only eliminates app store barriers and employs a conversational user interface—more intuitive than complex forms—to enable low-friction access, but its premium structure supports pay-as-you-go options, reflecting the irregular income streams of many small and micro business owners. Simultaneously, by operating on trusted communication platforms, it reduces the formality and intimidating nature often associated with insurance, building trust through familiarity.

The success of this model lies in its “invisible technology” approach. The advanced artificial intelligence and regulatory technology powering it operate behind the scenes, while the user experience remains simple, social, and conversational. It transforms insurance from an intimidating contract into a convenient chat, directly addressing challenges of trust and complexity. This case offers a replicable blueprint for other markets: leveraging ubiquitous social platforms to deliver formal financial services in an informal, accessible manner.

Figure 3: Araba Hollard user journey diagram

4. Suggestion

To enable insurance technology innovation to sustainably scale and deepen financial inclusion, coordinated action by all ecosystem participants is required.

Figure 4: Insurtech ecosystem collaboration diagram

For insurance technology startups and established insurers, the first step is to adopt human-centered, scenario-based design, developing solutions for specific high-pressure points in the journey of small and micro enterprises. Examples include “out-of-stock insurance” for retailers tied to inventory financing, or “late payment insurance” for contractors. Second, establish strategic data partnerships with mobile network operators, fintech companies, and utilities to build comprehensive, non-traditional risk assessments. Invest in cultivating local data science capabilities to interpret this data within Ghana’s context. Simultaneously, prioritize transparency as a core product feature by implementing and prominently promoting direct, rapid claims processes.

For regulators such as the National Insurance Commission and the Bank of Ghana, it is essential not only to expand and formalize regulatory sandboxes, creating a clear, accelerated pathway for products that successfully pass sandbox testing to scale up to full operations and provide regulatory certainty for innovators(National Insurance Commission). They must also champion industry utilities, promoting the development of shared, secure infrastructure—such as a universal fraud database or decentralized identity verification platforms—to reduce compliance costs and risks for all participants. They should also spearhead financial and digital literacy campaigns, collaborating with insurtech firms and community organizations to co-create educational content that explains insurance concepts in local languages and contexts, thereby building a more informed consumer base.

For international development partners and investors, funding can be directed toward applied local research, supporting collaborative studies between universities, insurtech companies, and local insurers to investigate highly localized risks (e.g., crop yields in Bono East, fishery health in Elmina) and develop corresponding parametric insurance models. Flexible, patient capital can also be deployed to build investment structures that account for the longer gestation periods required to establish trust and scale in inclusive finance. This approach moves beyond pure venture capital models to incorporate blended finance and impact-first funding.

5. Conclusion

The evolution of Ghana’s insurtech sector is not merely a technical subplot; it is a pivotal economic narrative about building systemic resilience. By leveraging the nation’s digital finance leap, innovators are weaving a digital safety net for millions of small businesses and individuals who underpin the economy. The ultimate success of this movement will hinge on sustained commitment to context-driven innovation, collaborative ecosystem building, and regulation that both protects consumers and empowers pioneers(Ghana Ministry of Finance). Ghana’s experience offers a vital lesson for the Global South: true financial inclusion is achieved when technology is applied not to disrupt, but to connect, protect, and empower the grassroots of the economy(National Insurance Commission).

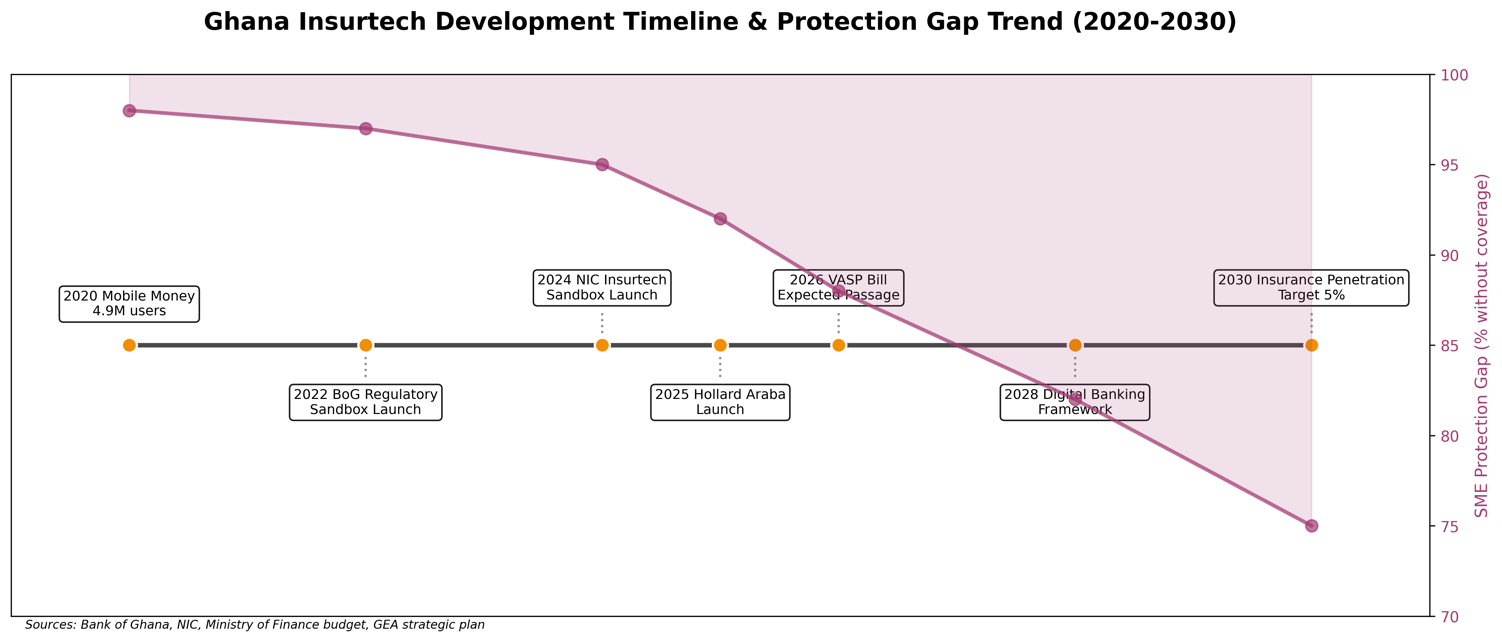

Figure 5: Insurtech impact timeline and protection gap trend

References

Bank of Ghana. Summary of Economic and Financial Data (October 2025). Bank of Ghana, 2025.

Ghana Ministry of Finance. Medium-Term Revenue Strategy. Government of Ghana, 2025.

Ghana Statistical Service. Ghana 2023 MSME Survey Report. Ghana Statistical Service, 2023.

Hollard Insurance Ghana. Case Study: Araba Hollard – Pioneering Virtual Insurance in West Africa. 2025.

National Insurance Commission. Guidelines for InsurTech and Digital Insurance Operations. National Insurance Commission, Ghana, 2024.

Ofori, Ebenezer, et al. Evaluating effective coverage of the National Health Insurance Scheme in Ghana: A mixed-methods study. BMC Public Health, vol. 25, no. 1, 2025, p. 450.

Author Biography

Junjie Guan holds a Bachelor of Economics from Harbin Institute of Technology, specializing in fintech and data analytics. Her research encompasses AI-driven credit risk prediction and dynamic ESG assessment frameworks. She possesses strong Python programming and machine learning model-building capabilities. Currently, as an intern at AAE, she engages in insurance technology and inclusive finance research and practice, dedicated to exploring how technology can provide solutions for sustainable development in emerging markets.